Federal Agency for Education

Department of Accounting and Audit

By discipline

"Economical geography"

"Characteristics of the Central Federal District"

Ekaterinburg

Introduction…………………………………………………………….3

1. general characteristics Central Federal District………… ……5

2. Economic characteristic Central Federal District ... ... 9

3. Problems and development prospects………………… ……21

Conclusion…………………………………………………………..32

Bibliographic list……………………………………….34

Attachment 1.

Appendix 2

Appendix 3

Appendix 4

Introduction

The Central Federal District unites the Central and Central Black Earth economic regions.

According to the administrative-territorial composition, it includes the city of Moscow and 17 regions: Belgorod, Bryansk, Vladimir, Voronezh, Ivanovo, Kaluga, Kostroma, Kursk, Lipetsk, Moscow, Oryol, Ryazan, Smolensk, Tambov, Tver, Tula, Yaroslavl.

The territory of the district belongs to central Russia with its characteristic relative unity of natural, geographical, demographic and economic features of development.

During the period of formation and development of market relations, the Central Federal District stands out among other territorial units of Russia with a more successful course of economic reforms aimed at a socially oriented, multi-structural market economy and structural restructuring. The Central Federal District provides the largest share of financial resources to the country's budget.

According to the localization coefficient, the branches of specialization of the Central District can be considered oil refining, ferrous metallurgy, chemical and petrochemical, mechanical engineering and metalworking, building materials industry, glass and porcelain-faience, light, food, flour-grinding industries.

The Central Federal District occupies one of the first places in the Russian Federation in terms of industrial output: a large number of engineering and metalworking products are produced here, a significant share of chemical products. The Central District is Russia's main producer of cotton, linen fabrics, and leather footwear. The district accounts for more than 90% of all printed products produced in the country. It is the main center for the development of science and culture in Russia, a forge of qualified personnel. In the interdistrict division social labor The Central District acts as the most important industrial center of the country.

The Central Federal District is a metropolitan region, leading in terms of population, economic and social development, having a complex differentiated economic structure and a dense network of railway and highways.

1. General characteristics of the Central Federal District

1.1. Geographic location of the Central Federal District

The Central Federal District occupies an area of 652.7 thousand square meters. km. The administrative center of the district is the city of Moscow (Appendix 1.).

At all stages of the development of the Center, a large place in determining its fate was occupied by geographical position. It is located at the intersection of water and land roads, which have always contributed to the development of economic ties, because even in ancient times the main trade routes crossed here. And at present, the position of the Center is in the middle of the most densely populated and economically developed part of the country, in the largest knot transport routes, at the "crossroads" of the most important economic ties between various territorial units, has a very great influence on the entire course of development of this district. The presence of the capital region also has a huge impact on the development of the regions of the Central Federal District. Moscow has developed economic, cultural, scientific, transport, supply and other ties with the regions of the region.

The Central Federal District borders on Belarus and Ukraine, and is also conveniently located in relation to the fuel and energy bases of the Volga region and the North Caucasus, with which economic relations are developing and interregional associations are formed.

The natural conditions of the region are characterized by moderate continentality, average temperatures in July +19 +22°С, January -8 -11°С, the amount of precipitation ranges from 400 to 550 mm per year, the duration of the growing season is 175-185 days. Despite the aridity of some parts of the region, conditions are favorable for agriculture. The relief is expressed by the Central Russian Upland and the Oka-Don Lowland. The area is poor in water resources, which is unfavorable for its economic development. The surface water sources of the region are represented by an extensive river network belonging to the basins of the Caspian, Black and Baltic Seas. Resource availability surface water area decreases from north-northwest to south-southeast. The land resources of the region are used very intensively. The degree of agricultural development of the territory is high.

1.2. Social aspect

In terms of population, the number of cities and towns, the variety of types and appearance of settlements, the Center occupies a special place in our country.

The population living on the territory of the Central Federal District is about 37.1 million people, or 20.4% of the population of all of Russia. In terms of population density (62 people per 1 sq. km.), Central also ranks first among all federal districts of Russia. The most densely populated are the Moscow, Tula, Ivanovo, Ryazan and Lipetsk regions, the lowest density is in the Tambov region. Almost the entire territory of the district is characterized by natural population decline, low birth rate, but due to intensive migration processes, there is an increase in numbers. The mechanical movement of the urban population is characterized by a large proportion of migrants from other economic regions. The central region south of Moscow is one of the main fields of migratory gravity. In exchange with Moscow and the region, almost all regions of the region are losing part of their urban population. Along with this, the mechanical increase in the urban population of these regions is formed mainly due to the influx of local rural residents. IN last years there has been a significant influx of refugees, especially to the rural areas of the southern part of the district.

Occupying an insignificant part of the territory of Russia, the Central District is distinguished by a particularly large population. Such a high population is determined by the historical factor. The center is the area of the most ancient Slavic settlement, the historical core of the Russian people. And at present, the region is distinguished by a very homogeneous national composition: the Russian population prevails here everywhere. There are small national groups in the east Ryazan region(Tatars) and northeast of Tverskaya (Karelians). In the southern part, the percentage of Ukrainians is quite high.

Characteristic Central Federal District - a high proportion of the urban population - 83% (Appendix 2). At the same time, the Ivanovo, Tula and Yaroslavl regions reached the average district indicator, and the Moscow region exceeded it. There are more than 30 large cities in the region, the share of the population of which in the total number of inhabitants of the Central District is almost half, and in the urban population - more than 2/3. In the Center, both large clusters of urban settlements and single cities and towns are common. Among the clusters of cities, Moscow occupies an outstanding place, around which a whole galaxy of satellites has grown. 1/2 of the urban population of the district lives in the Moscow agglomeration. Other major urban agglomerations, "millionaires" - Tula and Yaroslavl. An important reason for strengthening communication between the cities of the Okrug is their diversity, the special role of industry, territorial proximity, and favorable transport conditions. Large cities are characterized by high growth rates, which is due to the concentration of industry and social infrastructure. The network of urban settlements of the Center took shape over many centuries. Here, more than anywhere else, cities that are among the most ancient in our country have been preserved. It was they who became the reference points of modern urban settlement. Ancient cities (Smolensk, Ryazan, Vladimir, Vyazma, Kolomna) also predominate among the administrative and industrial centers. The Central District is characterized by a relatively small proportion of rural residents in the total population - 17%. The main reason for the reduction in the number of rural residents of the region is the intensive outflow from the countryside.

The demographic situation that has developed in the Central Federal District is characterized by low natural growth and an increase in the proportion of the population of older ages. The number of labor resources is insufficient. The population of the Center, as the ancient economic core of the country, has historically become the bearer of many diverse production skills. Thanks to early development industry, which relied on the existing skills of the population, in the Center, long before the revolution, a big army skilled workers. The district, primarily due to Moscow located within it, has played and continues to play an outstanding role in the development of culture and the training of qualified personnel. Higher than the national average, the level of employment of labor resources in the non-manufacturing sector is due to the role that the Central District plays in the development of science, culture and training of specialists. But the area itself is experiencing a shortage mainly in less skilled labor.

CFD budget

CFD budget- the budget of a certain financial responsibility center (FRC), a document whose indicators reflect the financial and economic activities of the employee or unit responsible for it.

Budgeting by the financial responsibility center is carried out by itself with the methodological support of the financial and economic service. Forms of budgets of the Central Federal District are developed in the course of budgeting. Their change is possible with the subsequent implementation and automation of budgeting, but in terms of volume it is usually insignificant if the enterprise approaches the formulation properly.

The appearance of the budgets of the Central Federal District in the company's activities is necessary for the implementation of budgeting. The lack of budgets of the Central Federal District allows us to say that budgeting has not been implemented at the enterprise, since the employees of the enterprise have no financial responsibility. The budget of the respective center includes items of activity in which the CFD participates or may be influenced. The starting point for motivating the personnel of the Central Federal District is the data of its budgets, both planned and actual. The financial responsibility center does not necessarily calculate the amount of expenses or income / payments or receipts. Its budget in form can be an income-expenditure budget (BDR), a cash flow budget (BDDS) or a balance sheet budget (BBL) of a given CFD.

For example, payroll can be conducted by the accounting department, the economic department and taken into account in the BDDS of the accounting department or the economic department. At the same time, wages for the BDR are included in the budgets of the corresponding Central Federal Districts; the budget of the Central Federal District, namely the BDR of the Central Federal District, which includes the accounting department or the economic department, contains only wages directly from the accounting department or the accounting department.

CFD

financial responsibility center

fin.

A source: http://www.1cbit.ru/management/glossary.php

- CFORF

Central Federal District;

Central Federal District Russian Federation

CFD

financial support center

Ministry of Internal Affairs of Russia

fin.

A source: http://40.mvd.ru/umvd/structure/item/737083

CFD

stock exchange center

organization, fin.

Examples of using

ZAO CFD "Trader"

CJSC CFD "Tant'ema"

. Academician. 2015 .

See what "CFD" is in other dictionaries:

CFD- Central Federal District Center Federal District Moscow Territory area 650.7 thousand km² (at the end of 2007) (3.82% of the Russian Federation) Population 37,121,812 people. (as of January 1, 2009) (26.16% of the Russian Federation), including: urban 29,994,175 people. rural 7,127,637 people. Density ... Wikipedia

- "Self-regulatory organization of arbitration managers of the Central Federal District" non-profit partnership http://www.paucfo.ru/ Moscow, organization ... Dictionary of abbreviations and abbreviations

Radio Frequency Center of the Central Federal District http://rfc cfa.ru/ communication ... Dictionary of abbreviations and abbreviations

Financial Reporting Center- (CFD) Structural units (workshops, production) for which plans are formed and which report on the results of the implementation of plans ... Vocabulary: accounting, taxes, business law

CFD CFORF Central Federal District; The Central Federal District of the Russian Federation of the Russian Federation ... Dictionary of abbreviations and abbreviations

Limit- (Limit) Contents Contents Definitions of the described subject Limitation banking operations Position Volume limits Limits on position characteristics, weighted volume Structural limits (share limits, concentration limits) Limits… … Encyclopedia of the investor

Public Chamber of the Central Federal District- Civic Chamber of the Central Federal District ... Wikipedia

Russian Church of Evangelical Christians- Protestantism Reformation Doctrines of Protestantism Pre-Reformation movements Waldenses ... Wikipedia

Kaluga region- Coordinates: 54°26′ s. sh. 35°26′ E / 54.433333° N sh. 35.433333° E etc. ... Wikipedia

Radio Seim- Radio "Seim" (AUKO TRC "Seim"). The direction of broadcasting is informational: politics, economics, Agriculture, social sphere, medicine, crime, accidents, culture, music, history, sports. All aspects of the life of Kursk and the region you ... Wikipedia

Books

- The effectiveness of managing the socio-economic development of administrative-territorial entities. Monograph. Dukanova I. V., Morozova T. N., Sukovatova O. P. , Dukanova I. V., Morozova T. N., Sukovatova O. P. Methods for assessing the level and potential of socio-economic development of administrative-territorial entities countries (regions and municipalities) as a key… Buy for 1176 UAH (only Ukraine)

- Efficiency of management of socio-economic development of administrative-territorial formations, Terekhin V.I. Methods for assessing the level and potential of socio-economic development of administrative-territorial formations of the country (regions and municipalities) as a key…

How to build the financial structure of a company, consisting of CFR (financial responsibility centers). This structure allows you to evaluate business performance, understand who is responsible for what, and develop a system of employee motivation.

From the article you will learn:

Does the company need to streamline management processes and set up a management accounting and budgeting system? First you have to build a foundation - the financial structure of the organization. It is a hierarchical system of financial responsibility centers (FRC) and determines the procedure for the formation of financial results, as well as the distribution of responsibility for achieving the overall result of the company.

Such structuring allows you to track the movement of resources within the company, evaluate the effectiveness of the business as a whole and its components. In other words, the presence of a financial structure allows management to see who is responsible for what, allows you to evaluate, control and coordinate the activities of departments, helps to develop an effective system of employee motivation.

CFO is...

The Financial Responsibility Center is structural subdivision an enterprise that is responsible for achieving quantitative results. He is also responsible for the distribution of responsibilities within the framework of achieving goals. Translated into English - financial responsibility center or simply responsibility center.

Types of CFD

The main types of CFD are presented in Table 1.

The key distinguishing feature of the center is the targets to which their activities are oriented. CFAs of different levels form a hierarchy in which, for example, a profit center may include revenue centers, cost centers of both types, as well as other profit centers. In turn, the profit center can be included in the investment center and other profit centers as a subordinate CFD.

Table 1. Main types of CFD

|

Performance indicators |

May include CFD |

May be included in the CFD |

|

| Revenue Center | income received from the activities of the Central Federal District | revenue center | profit center |

| profit center | profit received from the activities of the Central Federal District | centers of income, standard costs, costs, profits | profit and investment centers |

| Standard Cost Center | CFD costs per unit of product or service | standard cost center | centers of standard costs, and profits |

| Cost Center | CFD costs | standard cost and cost centers | profit and cost centers |

| Investment Center | return on investment (ROI) | centers of income, costs, profits, investments | investment center |

How is financial structure different from organizational structure?

The financial and organizational structures do not match. If the discrepancy between them is large, then serious managerial problems arise. The business vision that forms management accounting based on the FRC does not coincide with the enterprise management structure. In order for the enterprise management system to be adequate to the business, the organizational structure must be brought into line with the financial structure. The main differences between financial and organizational structures come down to three points:

- financial is built on the basis of economic and financial relations between responsibility centers. The organizational structure is based on the functional specialization of the organization's divisions. For example, costs of a certain type are grouped at the cost center, and functions are grouped in the organizational structure unit, the implementation of which requires certain professional knowledge and skills;

- CFD reflect the hierarchy of responsibility for achieving the target financial indicators. Organizational structure - hierarchy of subordination;

- at building an organizational structure “political” compromises and the influence of personal factors are possible. When building a financial one, only the realities of the business are taken into account.

requires a deep knowledge of the business and a willingness to look at the company" open eyes". For its formation it is necessary to determine:

- business structure;

- key processes;

- boundaries of investment activity;

- assets;

- profit structure;

- main managerial connections.

Development of the financial structure

Step 1. Determining the structure of the business

The first step to forming a financial structure is to determine the structure of the business. Often in one company several activities are combined that use common resources and are hardly distinguishable in the organizational structure. To highlight them, you need to consider the customer base, products and services. Here characteristics different lines of business:

- different groups of products are sold to different groups of customers;

- the company has different competitors for different product groups;

- Fundamentally different technologies and resources are used to produce different groups of products or services.

The presence of these signs indicates that the company operates not in one, but in two or more target markets, which have different target groups customers and different competitive conditions.

Often new directions of activity appear imperceptibly for a management. The situation becomes clear only as a result of analysis. For example, an enterprise producing transformer substations began to provide its customers with installation and connection services for these substations. The emergence of this service led to the creation of departments for the design, management construction work, maintenance and operation of construction equipment. The development of the service has led to the fact that complex projects for the construction of turnkey substations have become an independent product, more profitable than the traditional products of the enterprise. The realization that this is a new business did not come immediately. Figure 1 shows the top level of the financial structure of this company.

Picture 1

Step 2. Identify key processes

The next step is to analyze the process structure for each line of business. We are not talking about their detailed study and description. It is enough to highlight the key top-level processes in order to clarify the structure of the company's activities and associate responsibility centers with them. As a basic model for analysis, it is convenient to consider the "value chain" created for the client, as well as auxiliary groups of processes that ensure the functioning of the "value chain". An example of the key processes of a software development company is shown in Figure 2.

Figure 2. An example of key processes developing software

Consideration of the process diagram allows you to determine how the financial result is formed in this business and what are the main areas of investment for its development. On this basis, the main elements of the financial structure of the direction under consideration are formed. In the example under consideration, the centers of responsibility for groups of processes that form value for the consumer are clearly visible:

- purchase of components used to manufacture the product (CDs, program protection keys, packaging);

- production and packaging of the product;

- promotion of the product on the market (informing potential consumers about the capabilities of the product);

- product sale;

- technical user support.

The processes serving the main activity include the work of the legal department, accounting, maintaining the company's own IT infrastructure, and economic support. The main "value chain" also does not include the processes of company management. Special place takes development software. It refers to investment activities, since the creation of new products is aimed at business development.

It is important that the financial structure reflects the business model and becomes the basis for setting up clearly structured management accounting and building budget model. The structure of the FRC corresponding to these processes is shown in Figure 3. It shows how the centers of financial responsibility "Sales" and "Services" are responsible for the income from the sale of products and technical support services, respectively. CFOs "Production", "Purchasing" and "Promotion" are responsible for the costs of the processes under their jurisdiction. Their results form the overall result of the activities of the CFD "Production and Sales", which is the center of profit. Its profit is an indicator of all the production and commercial activities of the company. Net profit is formed taking into account the costs of the CFD "Maintenance" and "Management". The costs of the FRC "Software Development" do not affect profits, since the budget for the development of software products is financed not from current income, but from profits or external investments.

Figure 3

Step 3. Determination of processes related to investment activities

The question of what processes to attribute to investment activity, upon closer examination, turns out to be quite difficult. His decision has a direct impact on the financial structure. So, in the activity of a software developer, there are two directions:

- development of new products;

- support of products created earlier and distributed on the market.

The first direction, of course, refers to investment activities. The second is related to the maintenance of an asset already available to the company - a previously created software product. The maintenance process includes correcting errors in the program code identified during the operation of the program, making minor improvements at the request of users, and finalizing the documentation. This work can take 40-60% of the resources of the development department. Therefore, the decision of the question of what type of activity we attribute the costs of these resources to - investment or operating - will significantly affect the profit indicator. If the development and maintenance processes of software products are clearly delineated, then the best solution would be to present them with different responsibility centers, as shown in Figure 4.

Figure 4. Separation of responsibility centers

However, in practice, the processes of developing and maintaining software products are closely intertwined. It is not possible to ensure their separate accounting. Therefore, you have to make one of the following decisions:

- all activities of the development department are attributed to the CFD "Software Maintenance". This is acceptable if the company mainly distributes previously developed software products and does not invest heavily in new developments;

- all activities of the development department are attributed to the CFD "Software Development", that is, to investment activities. Such an assumption is possible if the company carries out a large amount of development;

- to divide between two CFDs those resources that can be unambiguously attributed to them, and to distribute the rest on the basis of peer review. In this case, employees who are engaged only in product maintenance will fall into "Maintenance", and developers of new products - into "Software Development". Those who are employed in two processes will be "divided" between the two CFDs in accordance with the assessment of their employment in these processes.

Such a division does not mean a mandatory change in the organizational structure. It is not people who are divided, but the resource of their working time and the corresponding costs. At the same time, the correct delineation of processes, which is necessary to build the correct financial structure and form adequate management accounting on its basis, will encourage managers to optimize processes and organizational structure.

Step 4: Defining Assets

Assets are long-term renewable resources of a company. They are created in the course of investment activities and "work" in business for a long time, providing a profit. It is very important to reflect assets in the financial structure - in connection with them, important decision-making questions always arise:

- how much did we invest in creating the asset?

- What does it cost us to maintain an asset?

- what is the return on the asset?

What kind of resources to attribute to assets is a question, the solution of which largely depends on the views of business leaders, their strategy and management style. Let's start with traditional look assets on the example of a development company that owns a business center building. This company operates in two lines of business:

- construction of objects for sale (hotels, shopping and entertainment complexes);

- leasing offices in the building of its own business center.

The top level of the financial structure that reflects these lines of business is shown in Figure 5. Obviously, with such a financial structure, it will not be possible to answer shareholders' questions about how much the "business center" asset they own costs, what are the costs of maintaining it and what is the return on the capital invested in it. The asset in this structure is not visible at all. It is "on the balance sheet" of the Central Federal District "Real Estate Rental Services". Although in fact it is the property of the owners of the company, transferred to the management of the business unit. That is, the structure does not reflect real ownership relationships and does not provide answers to key questions regarding the efficiency of asset use.

Figure 5

The situation is clarified in Figure 6. In this option, the profit center “Assets. Business center". It includes the cost of operating the building, depreciation of the asset, property taxes. The income of the CFR is formed from the fee for the use of the asset received from the CFR “Real Estate Leasing Services”. He acquires the right to use the building at a "wholesale price" (it is advisable to tie it to the market price), and sells it at retail to customers he finds on the market. He is also responsible for providing a range of services to tenants. Now the structure clearly clarifies the relationship of all parties interested in this business and makes the corresponding financial flows explicit. You can directly determine the return that assets bring, as well as the return on investment. The added value created by the CFD “Real Estate Rental Services” has become transparent due to its ability to attract customers and provide them with quality services.

Figure 6. Financial structure with a profit center “Assets. Business center"

Assets can include not only material objects, but also intangible business resources, such as a brand, information systems, and intellectual capital. Their inclusion in the financial structure only makes sense if these resources are truly managed as assets. The key difference between approaches to resource and asset management was noted by P. Drucker: “Resource costs need to be reduced, and investments in assets should be increased.” I will add that in this case, of course, it is necessary to evaluate the return on investment.

Step 5. Identification of the stages of profit formation

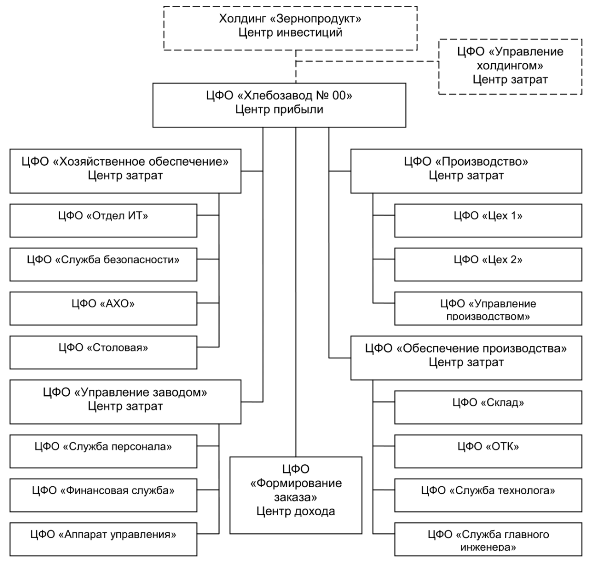

Profit is a universal indicator of the effectiveness of the company and its individual divisions. Approaches to , structuring methods affect the formation of the financial structure. Consider a bakery that is part of the grain holding system. The holding centralizes the functions of selling products and purchasing the main raw materials. The holding's management evaluates the plant's performance in terms of profit. At the same time, several stages of profit formation are distinguished, as shown in Figure No. 7:

- marginal profit serves as an indicator of the efficiency of the main production processes. When calculating it, conditionally variable costs are taken into account, which consist mainly of piecework wages and the cost of raw materials and materials;

- production profit characterizes production activity as a whole. It takes into account semi-fixed costs for the salary of production personnel, maintenance industrial premises, maintenance of production equipment;

- a controlled contribution to profit is the financial result of the bakery. When calculating it, all costs that are controlled by the plant management are taken into account. In addition to those listed above, this includes expenses for the maintenance of the administrative apparatus and economic support;

- gross profit is determined taking into account the share of the holding's expenses, which is imputed by the higher management to this business unit. These are the costs of maintaining the holding's management company, distributed among profit centers according to established rules;

- net profit is formed after the deduction of income tax and interest on loans from gross profit.

Figure 7

Each stage of profit formation is associated with a certain group of costs. It is necessary to allocate responsibility for various cost groups between financial responsibility centers - this will allow you to get an idea of the effectiveness of all the main production processes and manage them (see Figure No. 8). Here, responsibility for different kinds costs that determine certain stages of profit formation.

Figure 8. Distribution of responsibility for different cost groups

In a visual form, the scheme of delimitation of responsibility for cost groups is presented in Table 2. It can be seen from it that the production CFD “Workshop 1” and “Workshop 2” are responsible for the costs that consist of the piecework wages of workers, the cost of raw materials and materials used in production. CFD "Management of production", "Warehouse", "OTK" are responsible for the cost of wages of production personnel, maintenance of production facilities, maintenance of production equipment. CFO "Holding Management" is responsible for the costs of maintaining the holding's management company and taxes.

Table 2. Delimitation of responsibility for cost groups

| CFD | CFD |

variable costs |

fixed costs | Indirect domestic | Indirect external | taxes and interest |

| "Production" | "Workshop 1" | |||||

| "Manufacturing control" | ||||||

| "Workshop 2" | ||||||

| "Production Assurance" | "Warehouse" | |||||

| "OTK" | ||||||

| "Technologist Service" | ||||||

| "Chief Engineer Service" | ||||||

| "Economic support" | "Warehouse" | |||||

| "OTK" | ||||||

| "Technologist Service" | ||||||

| "Chief Engineer Service" | ||||||

| "Factory management" | "Warehouse" | |||||

| "OTK" | ||||||

| "Technologist Service" | ||||||

| "Chief Engineer Service" | ||||||

| "Holding Management" |

Step 6. Highlighting links between departments

All processes of the company are interconnected - the results of one serve as resources for another. Therefore, it is always possible to single out “suppliers” of internal products or services and “clients” using them in their work inside it. Once these relationships are included in the economic model, internal profit centers will appear in the financial structure. Such a model of relationships will be called "self-supporting" or "internal outsourcing". They provide the possibility of using economic mechanisms to motivate responsibility centers included in the value chain.

As an example, consider a production and trading company that has three main divisions: trade, production, logistics. The company sells mainly products of its own production. The logistics division ensures the storage of products in the company's warehouses and their delivery to customers. In the simplest case, the financial structure of the enterprise has the form shown in Figure 9. In accordance with it, the CFD “Sales” becomes a profit center, the indicator of which is a controlled contribution to profit - the difference between income and costs for the implementation of sales processes. All other CFDs are cost centers that influence the formation of profits.

Figure 9

After a deeper examination of the essence of the relationship between the divisions of the company, it becomes clear that the Central Federal District "Production" is a supplier of products for "Sale". And the Central Federal District "Logistics" provides for the latter services for the storage and delivery of products. In the case of establishing internal tariffs for products and services, the divisions of the Central Federal District "Production" and "Logistics" become profit centers. But this is an internal profit resulting from the accrual by these FRCs of income from the sale of their products and services to the Sales financial responsibility center (see Figure 10).

Figure 10

The arrows in the diagram show sources of income for profit centers. CFD "Sales" receives income from the sale of products on the market, and the CFD "Production" and "Logistics" - from the "sale" of its products and services to an internal client. In this case, the profit of the CFD "Sales" is formed taking into account the cost of products purchased from "Production" and the cost of services purchased from "Logistics". Thus, "Sales" is already becoming important value generated by internal suppliers. After all, it directly affects the performance of the Central Federal District. In accordance with this model, "Sales" will necessarily study the cost structure of domestic suppliers, compare their prices with market prices and put downward pressure on domestic prices. This pressure will work to reduce production and logistics costs and increase the efficiency of the company as a whole.

Implementing in-house outsourcing is a complex task. Establishing "customer-supplier" relationships between departments of the company is not limited to the development of schemes. But if a decision is made to implement in the company economic methods management, then the model of internal outsourcing should be correctly reflected in its financial structure.

How to quickly test your knowledge? Take a quick test and verify your competence.

Thanks for taking the test.

We already know the result, find out for you ↓

Find out the result

Not sure about your answer? take a look at it and they'll tell you.

Step 7. Formation of the financial structure

In control theory, the following types are defined :

- divisional;

- functional;

- design;

- matrix.

In practice, they are rarely found "in pure form". So, in the above example of a production and trade holding, the divisional structure is the basis of management. The holding includes trade, production and logistics business units, endowed with significant independence. On closer examination, we will see that the “Sales” CFD includes several trading companies located in different regions, each of which is a profit center: “Sales A”, “Sales B”, “Sales C”.

At the same time, in addition to the divisional structure, the company's management system has a functional component. For example, how the promotion of products to target markets is organized. At the top level of management, this task is solved by the marketing department of the holding's management company. In addition, in each trading company there is a marketing department that provides promotion in the regional market. This division has dual subordination. In the divisional structure, it is part of a trading company. In the functional area, it is subordinate to the marketing department of the management company, which determines the goals and objectives of working on the market, approves plans and budgets, and controls their implementation. This dualism should be reflected in the financial structure, since in the context of the functional projection it is necessary to present budgets, generate reports, and “collect” costs.

What errors in the financial structure lead to higher costs and lower profits

Find out a solution that will help develop the financial structure of the company, correctly allocate responsibility for income and expenses between departments.

In the financial structure of the CFD shown in Figure 11, the Marketing Department is included in the hierarchy of financial responsibility centers, the top of which is Alfa Product. At the same time, all CFDs, represented by shaded rectangles, are functionally included in "Marketing" (indicated by a dotted line), which is not part of the hierarchical structure. This is another projection of the financial structure. In the functional projection, other components can be distinguished, for example, "Information Technology", "Security" and others.

Figure 11

For companies that have many of the same type of geographically distributed divisions, a matrix financial structure is typical. A simplified example of it is shown in Scheme No. 12, which shows a company engaged in servicing regional electrical networks. It includes electric grid enterprises (PES), each of which has in its structure territorial divisions - district electric grids (RES). All district production units are engaged in the same activities: maintenance and repair of electrical networks, as well as installation and maintenance of electricity meters.

In the functional projection of the financial structure, these areas are presented respectively as the CFD "Maintenance of networks" and "Electricity metering". Implementation of work on overhaul is under the jurisdiction of the PES; RES level is absent here. In the diagram depicting the financial structure of this company, the shaded boxes represent the centers of financial responsibility, located at the intersection of the territorial and functional projections. For example, CFR "PES 1" reads as follows. PES 1 includes the following profit centers (territorial CFD):

- "RES 1.1"

- "RES 1.2"

- "RES 1.3"

On the other hand, PES 1 includes the following functional CFDs:

- "Management" (cost center)

- "Maintenance of networks" (profit center)

- "Electricity metering" (profit center)

- Overhauls (cost center)

To identify all managerial links, it is necessary to consider not only the functional and territorial aspects of management, but also to determine the principles for organizing project activities, which occupies a significant place in most companies.

Having wondered what it is - Financial centers, and looking for information about it, you will most likely come across the fact that the specialists of the financial and economic block do not have a unanimous opinion on this matter.

Wanting to understand the issue in detail, it is worth starting with the obvious. So, the CFD is one of the organs of the financial body of an enterprise, responsible for a certain economic result, and, undoubtedly, influencing the financial performance of the company.

At the same time, the system of Financial Responsibility Centers is one of the elements of the financial discipline system, which guarantees an enterprise real responsibility for the financial and economic results of its work.

Speaking about the Central Federal District, it should be noted that the creation of internal financial centers. Responsibility at the enterprise is a serious step towards the creation of a correctly oriented system of enterprise budgeting. And if everything is done correctly, then this system will be based on the responsibility of departments for the implementation of budgets and linking to the motivation system.

Different organizational structures of enterprises also imply a different CFR system: a unit can consist of several Financial Responsibility Centers at once, as opposed to how several unrelated departments can represent one CFR. The main issue here is the tasks that are assigned to the CFD, depending on its type, and the result that each CFD must show.

Categorization of Financial Responsibility Centers

There are not so many scenarios of financial results, namely four types:

- Investment return;

- Income;

- Costs (expenses);

- Profit (profit).

Based on this composition of performance indicators, a categorization of types of CFD is formed

Revenue Center

Revenue Center is a structural financial unit that is responsible for income from its own activities. A common example is the sales department, which has a bunch of unsold products in its arsenal and the authority to sell them. Influencing revenue with the help of various pricing tools, such a CFD has practically no opportunity to influence its own costs, although its activities are certainly connected with them.

Free

consultation

expert

Natalia Sivorina

Consultant-analyst 1C

Thank you for your feedback!

A 1C specialist will contact you within 15 minutes.

- the direct opposite of the center of income. He can only influence his costs, which appear as a result of his activities. A situation is considered good when Cost Centers have planned expenses and no other expenses arise.

Such a Center may have no income at all within the budget, and even the very procedure for budgeting at an enterprise provides that such a CFD should manage its costs and it is desirable to minimize them. A caveat is necessary here: a minimum of costs while maintaining the level of result, and not vice versa.

A good example of a cost center is HR: big budget, often low budget efficiency, almost no budget optimization and productivity improvement, and no revenue.

Note that among the classic Cost Centers there is also an internal typing

Standard Cost Center- this is a structure that controls only the norms for the consumption of various resources (money, screws, man-hours) calculated per unit of output. For example, if we began to sell very, very much, then our total budget for the provision of services or production of products (depending on our market) increases, but the standard must still be observed. This is the task of such a CFD. By the way, the standards are often deliberately overstated so that such CFDs can somehow maneuver in changing conditions.

Management Cost Center is the center of financial responsibility general level spending within your budget. The best example from the non-fictional world is the marketing and advertising departments. They spend a lot, often inefficiently, respectively, they are responsible for achieving results with adequate savings of the allocated budget. Simply put, their task is not to spend everything.

Investment cost center- this is, for example, a design department, whose task is to develop and produce new competitive types of products. In the long term, these investment costs are translated into product samples, which in serial production will provide the company with an opportunity to make a profit.

profit center- a division that affects both profits and expenses. It can influence its results, both by increasing income and reducing expenses, and one does not exclude the other.

Although it should be noted that in practice such a CFD may not always be responsible for net profit, because it is part of the enterprise and depends on the activities of other departments. Therefore, a subspecies of this CFD arises - Margin Center. The Center influences its revenues and its direct expenses, and is responsible for the effectiveness of its contribution to profits. But usually in life all such divisions are Profit Centers: each has its own type of profit.

– CFD, which is responsible for the return on investment in its activities, and its profit. Here, an important point is the ability of such a center to make decisions about investments and their directions, thereby increasing profits. Of course, in practice this is often not the case, but it is much more important that in such a CFD, investments are not a program imposed from above, but a method to achieve results. At the same time, it is important that the head of such a CFD be held responsible for the money invested and such indicators as the profitability ratio, payback period and added value. It is then that we can say that the unit is working correctly, like a real Investment Center.

The structure of Financial Responsibility Centers is a very complex and multifaceted concept, depending on a huge number of factors at each particular enterprise. Financial responsibility centers, of course, must be built into the overall hierarchical system of the organization, have the right relationships and be responsible to each other, without violating corporate rules and common sense.

At the same time, the most important task in structuring Financial Responsibility Centers is a clear distribution of functions and responsibilities, in which each CFO, regardless of its type, will understand what it is responsible for and what result is required from its work. This is the same financial discipline.

Formation and structuring of the correct interconnections of the Financial Responsibility Centers is not the easiest task for the company's management, but to solve it means to take a step towards civilized financial management and budgeting.