Macroeconomic equilibrium is a state of the national economy when the use of limited production resources to create goods and services and their distribution among various members of society are balanced. That is, there is an aggregate proportionality between:

- - resources and their use;

- - factors of production and the results of their use;

- - total production and total consumption;

- - aggregate supply and aggregate demand;

- - material and financial flows.

Conditions for economic equilibrium.

In a market economy, equilibrium is the correspondence between the production of goods and effective demand for them, that is, such an ideal situation when the product is produced exactly as much as they can buy at a given price. It can be achieved by limiting the needs for economic benefits, that is, by reducing the effective demand for goods and services, or by increasing and optimizing the use of resources.

This balance is an economic ideal: no bankruptcies and natural disasters, no socio-economic upheavals. In economic theory, the macroeconomic ideal is the construction of general equilibrium models of the economic system. IN real life there are various violations of the requirements of such a model. But the importance of theoretical models of macroeconomic equilibrium allows us to determine the specific factors of deviations of real processes from ideal ones, to find ways to implement the optimal state of the economy. In economic science, there are many models of macroeconomic equilibrium, reflecting the views of different directions of economic thought on this problem. Macroeconomic equilibrium is the central problem of social reproduction.

Distinguish between ideal and real balance.

The ideal is achieved in the economic behavior of individuals with the full optimal realization of their interests in all structural elements, sectors, spheres of the national economy.

Achieving such an equilibrium presupposes the observance of the following reproduction conditions:

- - All individuals must find consumer goods on the market;

- - All entrepreneurs must find factors of production on the market;

- - The entire product of last year must be implemented.

Perfect balance comes from the premise of perfect competition and the absence of side effects, which, in principle, is not realistic, since in the real economy there are no such phenomena as perfect competition and a clean market.

Crises and inflation throw the economy out of balance. Real macroeconomic equilibrium is an equilibrium that is established in the economic system under conditions of imperfect competition and with external factors affecting the market.

Distinguish between partial and complete equilibrium:

- - Partial equilibrium is called equilibrium in a particular market of goods, services, factors of production;

- - Complete (general) equilibrium is a simultaneous equilibrium in all markets, the equilibrium of the entire economic system, or macroeconomic equilibrium.

Full economic equilibrium is the structural optimum of the economic system, to which society strives, but never fully achieves it due to the constant change of the optimum itself, the ideal of proportionality.

Equilibrium can also be stable and unstable. An equilibrium is called stable if, in response to an external impulse causing a deviation from equilibrium, the economy independently returns to a stable state.

If after external influence the economy cannot self-regulate, then the equilibrium is called unstable. The study of stability and conditions for achieving general economic equilibrium is necessary to identify and overcome deviations, that is, to conduct an effective economic policy of the country.

An imbalance means that there is no balance in various spheres and sectors of the economy.

This leads to losses in the gross product, lower incomes of the population, the emergence of inflation, unemployment.

To achieve an equilibrium state of the economy, to prevent undesirable phenomena, experts use macroeconomic equilibrium models, the conclusions from which serve to substantiate the state's macroeconomic policy.

First of all, aggregate demand (AD, aggregated demand) is the sum of all individual demands for final goods and services offered in the commodity market. This also implies the following: aggregate demand is the aggregate expenditures planned by all macroeconomic entities for the purchase of all final goods and services created in the national economy. The concept of aggregate supply is equally important in macroeconomic equilibrium.

The aggregate supply (AS, aggregated supply) in economic theory is the sum of all final goods and services produced in the country that firms are ready to offer on the market for a certain period of time at every possible price level. In other words, this is the real volume of national production at different values of the price index for final goods and services.

The classical model of macroeconomic equilibrium.

The supporters of the classical approach assume that in conditions of perfect competition, full employment is achieved automatically. The scarcity of resources, in their opinion, highlights the problem of production, since, according to Say's law, aggregate demand always corresponds to aggregate supply. Therefore, the classical model studies the economy from the side of the aggregate supply. J. B. Say: "Products are exchanged for products."

The classical model of macroeconomic equilibrium prevailed in economic science for about 100 years, until the 30s of the XX century. It is based on J. Say's law: the production of goods creates its own demand. According to this theory, each manufacturer is also a buyer - sooner or later he buys goods produced by another person for the amount received from the sale of his own goods. Thus, macroeconomic equilibrium is ensured automatically: everything that is produced is realized. This model of this kind assumes the fulfillment of three conditions:

- - each person is both a consumer and a producer;

- - all producers spend only their own income;

- - the income is spent in full.

But in the real economy, a portion of the income is saved by households. Therefore, aggregate demand decreases by the amount of savings. Consumption spending turns out to be insufficient to purchase all manufactured products. The result is unsold surplus, causing a decline in production, higher unemployment and lower incomes.

In the classical model, the lack of funds for consumption caused by savings is compensated by investments. If entrepreneurs invest as much as households save, then J. Say's law is valid, the level of production and employment remains constant. That is, the generated volume of aggregate supply is the sum of household incomes, which are distributed by the latter for consumption and savings:

In order for an equilibrium to be established in the market of goods, the equality of the aggregate supply to the aggregate demand is necessary. Since the aggregate demand in the simple model represents the sum of consumer and investment expenditures:

Then, if the condition I = S is met, equilibrium will be established in the market of goods.

The main task is to encourage entrepreneurs to invest as much money as they spend on saving. It is solved in the money market, where supply is represented by savings, demand - by investments, price - by the interest rate. The money market self-regulates savings and investments with an equilibrium interest rate.

The higher the interest rate, the more money is saved (since the owner of the capital receives more dividends).

The second factor that ensures equilibrium is the elasticity of prices and wages. If, for some reason, the interest rate does not change with a constant ratio of savings and investment, then the increase in savings is offset by a decrease in prices, as producers seek to get rid of surplus production. Lower prices allow fewer purchases while maintaining the same level of production and employment.

In addition, a decrease in the demand for goods will lead to a decrease in the demand for labor. Unemployment will create competition and workers will accept lower wages.

Its rates will be reduced so much that entrepreneurs will be able to hire all the unemployed. In such a situation, there is no need for government intervention in the economy. Thus, classical economists proceeded from the flexibility of prices, wages, interest rates, from the fact that wages and prices can move freely up and down, reflecting the balance between supply and demand.

In their opinion, the aggregate supply curve AS has the form of a vertical straight line, reflecting the potential volume of GNP production. A decrease in price entails a decrease in wages, and therefore full employment is maintained.

There is no reduction in the value of real GNP. Here all products will be sold at different prices. In other words, a decrease in aggregate demand does not lead to a decrease in GNP and employment, but only to a decrease in prices. Thus, the classical theory believes that the economic policy of the state can only affect the price level, and not the volume of production and employment. Therefore, its interference in the regulation of production and employment is undesirable.

Keynesian model of macroeconomic equilibrium.

Keynesian proponents believe that in a market of imperfect competition, full employment can only arise by chance. Aggregate demand is unstable and, as a rule, insufficient to realize potential GDP.

As a result, the equilibrium GDP turns out to be lower than the potential one and, as a consequence, the incomplete use of resources. Particularly volatile, according to Keynesians, is the investment demand of firms.

J.M. Keynes criticized the assertion of the classics that investment necessarily coincides with household savings. He substantiated the possibility of actual inequality of investments and savings by the fact that they are carried out by different economic agents pursuing different goals and having different motives of behavior.

Investments are made by firms and savings are made by households. People make savings to buy high-value goods, to provide for old age, in case of unforeseen expenses, etc.

Firms, on the other hand, invest in order to make a profit.

The growth in household savings (and, accordingly, the reduction in their expenditures) is not always offset by an increase in investment expenditures. In this case, a reduction in aggregate demand leads to a drop in national production.

Under the conditions of underemployment, according to Keynesians, the main economic problem is not the problem of aggregate supply, but aggregate demand.

Keynes considered aggregate demand (aggregate spending) to be the main factor determining the value of aggregate supply. The more economic agents are willing to spend on the purchase of goods, the more products firms will want to produce. The Keynesian model, therefore, studies the economy from the side of aggregate demand.

According to Keynesians, the state is called upon to stimulate aggregate demand, to achieve its coincidence with potential GDP. J.M. Keynes and his followers proposed a set of measures of monetary and fiscal policy of the state aimed at stimulating aggregate demand.

Thus, the fundamental difference between the classical and Keynesian approaches is that the classics consider the aggregate supply to be the main factor of stable economic development, while the Keynesians consider the aggregate demand.

Unlike neoclassicists, J. Keynes proceeded from the fact that market macroeconomics is characterized by imbalance: it does not provide full employment and does not have a self-regulation mechanism. At the same time, J. Keynes criticized two fundamental theses of the neoclassical equilibrium theory.

First, he disagreed with the nature of the relationship between investment, savings and the interest rate. The point is that there is a mismatch between investment and savings. After all, the subjects of savings and investors represent different groups of the population, which are guided by different economic interests and motives. So, some make money savings in order to buy a house, others - land, others - a car, etc. The motives of investments are also different, which are not reduced only to the interest rate. Such a motive may be, for example, a profit that depends on the size and efficiency of the investment. It should be borne in mind that credit institutions can be a source of investment, in addition to savings. As a result, the processes of saving and investment are not aligned, which gives rise to fluctuations in the aggregate size of production, income, employment and price levels.

Secondly, the economy is developing inharmoniously, there is no elasticity of the ratio of prices and wages, as neoclassicists believe. This is where the imperfection of the market is manifested due to the existence of monopolistic producers. Under these conditions, according to J. Keynes, aggregate demand becomes volatile and prices become inelastic, which maintains unemployment for a long time. Therefore, government regulation of aggregate demand is necessary. According to J. Keynes, the amount of goods and services produced is directly dependent on the level of total expenditures (or aggregate demand), that is, the cost of goods and services. The most important part of total spending is consumption, which, together with savings, equals after-tax income (disposable income). Therefore, this income determines not only consumption, but also savings. In addition, the amount of consumption and savings depends on factors such as the amount of consumer debt, the amount of capital, etc.

The next component of total costs are investments, the amount of which depends on two factors: the real interest rate and the rate of net profit.

The amount of investment costs is influenced by the cost of acquiring, operating and maintaining fixed capital, changes in the availability of this capital, in technology and other time factors.

Thus, these consumption and investment expenditures, which determine the value of aggregate demand, are unstable. This causes instability in market macroeconomics.

To balance the economy, to ensure its equilibrium, it is necessary, according to J. Keynes, to have “effective demand”. The latter consists of consumption and investment costs. Effective demand should be maintained using a multiplier linking an increase in this demand with an increase in investment. economics economic Keynesian

In this case, each investment turns into an individual income for consumption and savings. As a result, the increase in "effective demand" becomes the multiplied value of the increase in the initial investment. Moreover, the multiplier is directly dependent on how much of the income people spend on consumption. But personal consumption grows with income, although to a lesser extent than income. This is due to a psychological factor in the desire of people to save. It is the latter, according to J. Keynes, that leads to a decrease in the share of consumption in total income.

Considering a decrease in the share of consumption in total income as a natural phenomenon inherent in human nature, J. Keynes notes that it is necessary to maintain such a component of total income as investment. Private investment should be supported by the state through tax, monetary policy and government spending.

In this way, the lack of "effective demand" is compensated by additional government demand, which contributes to the achievement of macroeconomic equilibrium. Inflation and unemployment are characteristic of modern macroeconomics. Prices and wages are in dynamics, they can decrease or increase.

Therefore, the aggregate supply curve AS does not have a strictly vertical and horizontal significance, as it is presented in the neoclassical and Keynesian general market equilibrium models.

It should be noted that the shape of the aggregate supply curve AS, depending on the change in AD, has not only theoretical, but also practical significance for stabilization and economic growth in the country. Thus, in the current crisis conditions in Russia, the Keynesian version of increasing aggregate demand AD, in which the growth of GNP is not accompanied by an increase in prices, is more appropriate. At the same time, the classical concept, when an increase in aggregate demand AD does not lead to an increase in GNP, but to an inflationary rise in prices, is not suitable.

Thus, the essence of Keynesian analysis is that an economy left to itself and functioning according to the principle of an "invisible hand" is very likely to find itself in a situation of either inflation or unemployment.

Once in this position, it is not able to come to equilibrium on its own, since in an economic system with rigid prices there is no internal mechanism that automatically balances aggregate demand and aggregate supply at the level of full employment. In the time of the classics, such a mechanism existed; it was a system of flexible prices, primarily flexible wages. If unemployment arose in the economy, wages decreased and the demand for labor increased until everyone who wanted to work found suitable jobs.

However, by the 1930s. on the labor market, the role and influence of trade unions has significantly increased, which have managed to significantly limit the opportunities for entrepreneurs to lower the price of labor.

Therefore, the economy of this period, having come to a state of equilibrium with underemployment, can stay in it for as long as desired, not showing the slightest tendency to involve unused resources in production, primarily free labor. Part-time employment is becoming sustainable.

Macroeconomic equilibrium concept

As you know, in any market economic system, all produced products must become goods, and all income must be spent on these goods. Only in this case, all these aggregate values (effective demand and aggregate supply) will coincide. This balanced state is called “macroeconomic equilibrium”.

Any economy can be in two mutually exclusive states: equilibrium and disequilibrium (dynamics). In other words, it is in constant motion, and therefore the equality of aggregate demand and aggregate supply is often violated. This is the reason for the emergence of macroeconomic imbalances: inflation, unemployment, production decline and balance of payments imbalance. And although this may be accompanied by very negative social consequences - through such deviations from equilibrium, the economy is in dynamics, which means it is developing.

Definition 1

Macroeconomic equilibrium- the balanced state of the economic system as a single integral organism and at the same time, the fundamental problem of macroeconomic analysis.

In a macroeconomic equilibrium, compliance should be achieved between the following basic economic parameters:

- aggregate demand and aggregate supply;

- production and consumption;

- savings and investments;

- commodity mass and its monetary equivalent;

- capital markets, labor and consumer goods.

The main condition for achieving macroeconomic equilibrium is equality between aggregate demand ($ AD $) and aggregate supply ($ AS $). That is, the equality $ AD = AS $ must be fulfilled (Fig. 1):

Figure 1. The classical model of macroeconomic equilibrium. Author24 - online exchange of student papers

As can be seen from Fig. 1, macroeconomic equilibrium is the “place” where demand ($ AD $) and supply ($ AS $) “meet”, intersecting at the point $ M $. This point means the equilibrium volume of production, and, at the same time, the equilibrium level of prices. Thus, the economic system is in equilibrium at such values of the real national product and such a price level at which the volume of aggregate demand will correspond to the volume of aggregate supply.

Types of macroeconomic equilibrium

Macroeconomic equilibrium can be of different types: partial, at the same time general and real.

Partial equilibrium is understood as equilibrium in individual commodity markets of the national economy. This type of macroeconomic equilibrium was studied in detail in his works by the famous economist A. Marshall.

At the same time, general equilibrium is equilibrium as a single interconnected system, which is formed by all market processes taking place in the economy.

Real macroeconomic equilibrium, as the name suggests, takes place in conditions of imperfect competition, as well as when external factors influence the market.

Remark 1

General macroeconomic equilibrium is considered stable if, after its violation, it is able to recover with the help of market forces. If active government intervention is required to restore equilibrium, then the equilibrium will be considered unstable. L. Walras is considered the founder of the theory of general economic equilibrium. According to Walras, in general equilibrium, balance is achieved simultaneously in all markets: consumer goods, money, labor market, etc. A necessary condition is the flexibility of the system of relative prices.

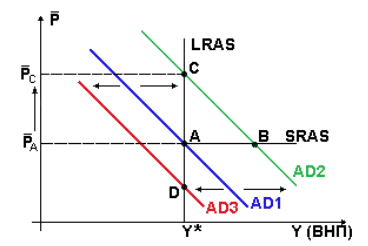

In an economic system, general equilibrium can be achieved both in the short term (intersection of the $ AD $ and $ SRAS $ lines) and in the long term (intersection of $ AD $ and $ LRAS $) (Fig. 2). In the short run, equilibrium is achieved by the economy with underemployment of resources. The long-term period implies equilibrium with full employment of resources (that is, with only a natural level of unemployment). General macroeconomic equilibrium implies that total expenditures correspond to the total volume of national production, and investments (I) are equal to savings ($ S $). In addition, the amount of demand for money must correspond to the amount of money supply in the economic system.

If the equilibrium in the economy, which is close to the state of full employment of resources (point $ A $ in Fig. 2), is caused by the change in aggregate demand from the position $ AD_1 $ to $ AD_2 $, the economy will first reach its short-term equilibrium (point $ B $) , and then reaches long-term (point $ C $). This striving of the economy to a state of stable equilibrium (to the point $ C $) occurs sequentially through price changes.

Figure 2. General macroeconomic equilibrium. Author24 - online exchange of student papers

A change in aggregate demand from the position $ AD_1 $ to $ AD_2 $ may occur, for example, due to an increase in the money supply in the economy. When a short-term equilibrium is reached (point $ B $), the price level remains unchanged for some time, since producers can increase supply at the expense of reserves, as well as involving additional reserve capacities in production. However, the continuing pressure of aggregate demand will continue to stimulate production growth. This will inevitably lead to an increase in average costs, since an increase in demand for resources in conditions of their full employment will contribute to an increase in the price of labor (wages).

Further, the increased average costs will begin to restrain the growth of production volumes, which will reduce the aggregate supply. In turn, this will increase the price of goods and services. This rise in prices will restrain the growth of aggregate demand (in Fig. 2, the value of aggregate demand decreases, moving along the $ AD_2 $ curve from point $ B $ to point $ C $). The final result of the adaptation of the economic system to the change in aggregate demand from $ AD_1 $ to $ AD_2 $ will be the achievement of a state of long-term equilibrium (at the point $ C $) with the same volume of national production, but already at a higher price level.

Economic practice confirms that regardless of the reasons causing the change in aggregate demand and the violation of the initial long-term equilibrium, in the long run the economy through self-organization, self-regulation returns to the level of potential GNP, given by the available amount of resources and technology.

In conditions of underemployment of resources, an increase in aggregate demand over a long period of time can stimulate an increase in the value of aggregate supply, up to potential GNP. However, further growth in aggregate demand will cause the reaction described above (Fig. 2).

In the event of a decrease in aggregate demand, caused, for example, by a decrease in the money supply or an increase in taxes, the $ AD $ curve will shift to the left, which will indicate a decrease in GNP in the short term at a constant price level. In the future, a downward price change due to an increase in unemployment, a decrease in wage rates (decrease in average costs), will gradually return the economy to the level of potential GNP (movement along the $ AD_3 $ curve to the $ D $ point). However, in the real economy, the prices of goods and the price of labor, due to imperfect competition, tend to rise to a greater extent than to decline, i.e. they are not “flexible” downward, so the volume of national production can recover at the potential level, but at a higher price level.

The life of a market economy can be characterized as a simultaneous stay in two mutually exclusive states: equilibrium and disequilibrium (dynamics).

In a market economy, all manufactured products (aggregate production) must become goods (aggregate supply), and all income (aggregate income) must be expended (aggregate demand) and purchased (aggregate consumption). Only in this case will the aggregate values of effective demand and supply of goods coincide. This ideal, but practically unattainable state of the market economy is its “economic equilibrium”.

On the other hand, the market economy is in constant motion, which causes a violation of the equality of aggregate demand and aggregate supply. And although each such deviation is accompanied by many negative consequences, it is only through such deviations that "economic dynamics" occurs - the development of a market economy. Let's consider these states in more detail.

Macroeconomic equilibrium- achieving in the national economy the balance and proportionality of economic processes: production and consumption, supply and demand, production costs and results, material and financial flows.

The main condition for achieving macroeconomic equilibrium is equality between aggregate demand and aggregate supply (AD = AS).

Macroeconomic equilibrium is the only price level at which the amount of aggregate products (goods and services) offered on the market is equal to the amount of aggregate demand.

Various areas of economic science have differently assessed the problem of achieving macroeconomic equilibrium. Let's briefly dwell on the most important of them.

The classical theory of macroeconomic equilibrium. Classical economists (A. Smith, D. Ricardo, J. B. Say, A. Marshall and others) believed that the market economy independently copes with the efficient allocation of resources and their full use. The main point of this theory is Say's law, according to which the production process itself creates income exactly equal to the value of the goods produced, i.e. supply generates its own demand (AD = AS).

The ability of a market economy to self-regulation provides the required level of production and employment automatically (although sometimes there may be disruptions in the economy associated with wars, droughts, political upheavals). Therefore, full employment is the norm of a market economy, and the best economic policy of the state is non-interference in the economy. These views dominated in economics until the 30s of the twentieth century.

Keynesian theory of macroeconomic equilibrium. The economic crises of the 1930s disproved the classical theory. The English economist John Maynard Keynes and his followers proved that the monopoly economy is characterized by imbalance, it does not guarantee full employment, and therefore does not have an automatic self-regulation mechanism.

Keynes considered aggregate demand to be volatile and prices to be inelastic (not having a tendency to decrease with an increase in sales), so unemployment can persist for a long time. Hence the need for a macroeconomic policy to regulate aggregate demand, which is very volatile. Keynes believed that for the economy to be balanced, to achieve equilibrium, demand must be “effective”. The state, by supporting private investment through tax, monetary policy and through government spending, compensates for the lack of “effective demand” with additional government demand and thereby helps the economy to approach the level of full employment.

Neoconservative theory. In the mid-1970s, industrial production growth declined in Western countries. This phenomenon was caused by:

a) another crisis of overproduction;

b) the onset (approximately 50 years after the end of the Great Depression) “downward” wave of the great cycle;

c) an increase in oil prices by the OPEC member countries by more than 4 times, which contributed to high cost inflation with a simultaneous decline in production, the so-called stagflation (a combination of stagnation in production with inflation).

Keynesian theory was also hit hard. It became obvious that active government intervention in the economy was not able to prevent a decline in production. This theory was replaced by a neo-conservative trend, which again advocated non-interference of the state in the economic activities of firms. A model of macroeconomic regulation was developed, based on the revival of market self-regulation and the stimulation of private entrepreneurship. In accordance with the recommendations of the neoconservatives, the economic policy of the USA, Great Britain, Germany and a number of other states was based on the principle of "effective proposal" - the encouragement of private business. In order to make free enterprise more profitable, taxes on profits and on labor income have been significantly reduced. The state noticeably reduced its interference in economic affairs, the partial privatization of state-owned enterprises began - their sale to private individuals, transformation into joint-stock companies. In many countries, the planning of the economy was noticeably curtailed, the financing of social programs was reduced. The measures taken made it possible to significantly reduce the state budget deficit, reduce the amount of money in circulation, while the inflation rate fell 3-4 times, and the rate of economic development increased.

But the model of neoconservative regulation of the economy did not save the West from declines in production and inflation. In 1979-1981. a new economic crisis broke out. The search for a new macroeconomic regulator has begun.

Mixed management. A critical comparison of the state (Keynesian) and market (neoconservative) regulators convincingly proved the inferiority of both exclusively market and only state economic mechanisms. The type of mixed management of the national economy was proposed by the laureate Nobel Prize Paul Samuelson (USA). This macroeconomic regulator has the following specific features.

1. it organically combines the stability of public administration necessary to meet public needs (social sphere, non-market sector), and the flexibility of market self-regulation, which is required to meet rapidly changing personal needs.

2. Mixed management allows you to optimally combine macroeconomic goals: economic efficiency, social justice and stability of economic growth.

3. The new regulator is able to balance aggregate demand and aggregate supply and thereby overcome the asymmetry of Keynesian concepts of effective demand and effective supply of neoconservatives.

This type of macroeconomic regulation prevails today in all developed countries with market economies, although there are various options for it:

With minimal participation of the state in the regulation of the economy (USA);

With the maximum admissible government regulation (Sweden, Austria, Germany, Japan, etc.).

Types of macroeconomic equilibrium:

1. General and partial balance. General equilibrium is understood as the interconnected equilibrium of all national markets, i.e. the balance of each market separately and the maximum possible coincidence and implementation of the plans of economic entities. When a state of general economic equilibrium is reached, economic entities are fully satisfied and do not change the level of demand or supply to improve their economic situation.

Partial equilibrium is an equilibrium in individual markets that make up the system of the national economy.

2. Equilibrium can be short-term (current) and long-term.

3. The balance can be ideal (theoretically desired) and real. The prerequisites for achieving perfect balance are perfect competition and no side effects. It can be achieved provided that all participants in economic activity find consumer goods on the market, all entrepreneurs find factors of production, and the entire annual product is fully realized. In practice, these conditions are violated. In reality, the task is to achieve a real balance that exists with imperfect competition and the presence of external effects and is established with incompletely realized goals of participants in economic activity.

4. Equilibrium can also be stable and unstable. An equilibrium is called stable if, in response to an external impulse causing a deviation from equilibrium, the economy independently returns to a stable state. If after external influence the economy cannot self-regulate, then the equilibrium is called unstable. The study of stability and conditions for achieving general economic equilibrium is necessary to identify and overcome deviations, i.e. to conduct an effective economic policy of the country.

An imbalance means that there is no balance in various spheres and sectors of the economy. This leads to losses in the gross product, lower incomes of the population, the emergence of inflation, unemployment. To achieve an equilibrium state of the economy, to prevent undesirable phenomena, experts use macroeconomic equilibrium models, the conclusions from which serve to substantiate the state's macroeconomic policy.

The analysis of equilibrium in the national market is carried out by combining the graphs of aggregate demand and aggregate supply in the same coordinate axes. The market system will be in a state of equilibrium if, at the current price level in the economy, the value of the estimated volume of production in the economy is equal to the value of aggregate demand.

The intersection of the curves of aggregate demand and aggregate supply, thus, will determine the equilibrium real volume of domestic production and the equilibrium level of prices in the economy. The presence of three specific areas on the aggregate supply graph complicates the analysis somewhat. Consider the situation of establishing macroeconomic equilibrium at each specific section of the AS chart.

The first case is the intersection of the graphs of aggregate demand and aggregate supply in the intermediate section of the latter. This case is the usual case when a change in the level of prices in the economy actually excludes overproduction and underproduction.

Macroeconomic equilibrium will be achieved at point E with the following parameters: P E - equilibrium price level in the economy; Q E is the equilibrium volume of production in the economy.

If the price level is higher than the equilibrium level, surplus products will appear on the national market. The presence of surplus (excess supply) will "push" prices down to the level corresponding to P E in the figure above. The opposite situation takes place if the price level in the economy is less than the equilibrium one. In this case, the economy will face the problem of a deficit in the national market. The shortage of products will allow to raise prices to the initial level, that is, to R E. The possibility of changing the price level in the economy practically nullifies the situation of overproduction and underproduction, this allows the market system to self-regulate and be in equilibrium.

The next variant of equilibrium between aggregate demand and aggregate supply will be considered on the Keynesian section of the AS graph (figure below). A feature of this version of macroeconomic equilibrium is that the price level throughout the Keynesian segment is unchanged and equal to P E. This means that prices, in contrast to the case considered above, here cannot be a tool to influence the market situation. If we assume that the economy produces more output than is demanded by the market, for example, QA (QA> QE), then the economy will face an increase in unsold inventories (by (QA - QB)), which will not be accompanied by fluctuations in the price level ...

In response to the growth of inventories, entrepreneurs will reduce production volumes, gradually bringing them to the level corresponding to point E. If the volume of production in this economy is less than equilibrium, for example, Q B, there will be a reduction in normal inventories. For producers, this will signal the need to increase production volumes, and the process of expanding production volumes will continue until the situation returns to normal, i.e. will not return to point E. All of the above allows us to conclude that in the Keynesian segment AS, it is the state of commodity stocks and their dynamics that act as a kind of indicator of the situation in the national market. Note that in both the first and second cases, macroeconomic equilibrium is achieved under conditions of underemployment and the equilibrium GDP turns out to be less than the potential GDP surplus to production.

And, finally, the last case is the equilibrium of the aggregate supply and demand on the classic section of the AS graph. This option means that macroeconomic equilibrium is achieved under conditions of full employment of economic resources.

The real volume of the domestic product here corresponds to the potential GDP, that is, the GDP in full employment (Q max). Full employment in the economy excludes overproduction and underproduction.

The situation of a stable market equilibrium at the level of the entire national economy is an exception rather than a rule, and is quite rare, since aggregate supply and aggregate demand are influenced by many factors.

A rapid change in aggregate demand or aggregate supply will disrupt the macroeconomic equilibrium. In the economic literature, abrupt changes in aggregate demand or aggregate supply are called, respectively, a demand shock and a supply shock.

A demand shock can arise, for example, as a result of a significant increase in the money supply (for example, the government could have resorted to issuing money to settle its debts). A demand shock can be caused by fluctuations in business investment activity (for example, in an economic upturn, investment costs increase sharply), and by the rush demand of the population, frightened by rumors of a possible price increase, and a sharp influx of imported goods (for example, as a result of the liberalization of foreign economic activity rules) and other reasons. A supply shock is most often due to a sharp change in production costs, which, in turn, may be associated, for example, with an increase in world energy prices, or with a large influx of immigrants, which sharply increased the supply of labor, or with the rapid introduction of new technologies and etc.

Let us first analyze how the change in aggregate demand will affect the equilibrium parameters of the national market. These figures illustrate the increase in aggregate demand.

Consider the option of reducing aggregate demand. If the economy is in a state of recession (Keynesian section of the aggregate supply graph), then a decrease in demand across the entire economic system will result in a decrease in production volumes and an increase in unemployment. The general level of prices will remain unchanged. Thus, we will be faced with a situation opposite to the case considered in the figure. By analogy, it can be assumed that when the AD and AS graphs intersect at the intermediate or classical parts of the aggregate supply curve, a downward change in aggregate demand should cause a decrease in the price level in the economy and the volume of GDP. However, practice shows that, having increased once, prices almost never fall to the previous level, even with a decrease in AD. If they decrease, it is insignificant. This is explained as follows.

1. The main component of the price of any product is production costs, most of which are wages. And the wage practically never decreases, that is, it is inelastic downward, since there is a statutory minimum wage; trade union organizations, defending the interests of their members, prevent the reduction of wages; the entrepreneurs themselves are afraid of discouraging labor productivity and losing their most qualified personnel.

2. The second reason for the inelasticity of prices downward is the significant monopolization of most modern

commodity markets and, as a consequence, the existence of the ability of monopolies to hold prices even with a decrease in demand for

market.

The situation described (associated with the inelasticity of prices to a decrease) is called the ratchet effect. Let's consider its graphic interpretation (see the figure below). Suppose that initially equilibrium in the economy was achieved at point A in the Keynesian section. Let us now assume that, for some objective economic reasons, the aggregate demand has increased and the curve AD 1 has shifted to the position of AD 2 on the plane. Equilibrium has moved from point A to point B, located on the classic section of the AS chart. Such a change in the macroeconomic situation led to an increase in the price level from P A to P B and increased the volume of real GDP from Q 1 to Q max. Further, suppose that under the influence of non-price determinants, aggregate demand decreased and the AD curve returns to its original position, that is, it shifts to the AD 1 level. Due to the ratchet effect, this change in aggregate demand will not lead to a change in the price level in the economy.

To preserve the equilibrium parameters, the Keynesian segment moves up to the position Р В В, and the aggregate supply graph itself will now be represented by the broken line P B BAS. Now the equilibrium of the economic system is achieved at point D, with the equilibrium parameters P in and Q 2.

The next stage of our analysis will be related to the study of the impact of changes in aggregate supply on macroeconomic equilibrium (see figure below). If, for any reason, the aggregate supply grows, this will be accompanied by an increase in the volume of national production (from Q A to Q B) with a general decrease in the price level (from P A to P b). This situation means an upturn in the economy.

In the event of a reduction in the aggregate supply in the economy, so-called supply inflation (cost inflation) will arise - a shift of the AS curve to the left upward to the position AS 2 will entail a simultaneous reduction in GDP (from QA to Q c), an increase in unemployment and an increase in the aggregate price level ( from P A to P s). Thus, the economic system will experience a decline in production (stagnation), accompanied by inflation. This situation in the economy is called stagflation.

In most cases, supply and demand shocks lead to inactive consequences. The state is taking a number of stabilization policy measures aimed at maintaining macroeconomic equilibrium and minimizing the negative consequences of shocks. These measures include elements of monetary and fiscal policy.

For your information. Considering supply and demand shocks, we found that with an increase in aggregate demand (in particular, in the vertical and ascending sections of the aggregate supply graph), the price level in the economy will increase. We will observe a similar increase in the price level with a reduction in aggregate supply. In fact, we are talking in the first case about demand inflation and in the second case about supply inflation.

Introduction

Chapter 1. Theoretical Foundations of Macroeconomic Equilibrium

Chapter 2. Models of economic equilibrium by D. Keynes

Conclusion

List of used literature

INTRODUCTION

Macroeconomic equilibrium is a state of the economic system, in which there is an equality of the volume of production and the volume of consumer demand.

In a market economy, the problem of macroeconomic equilibrium is of fundamental importance. Achieving macroeconomic equilibrium is closely linked to achieving full employment, price stability, and economic growth.

Different schools of economics have different views on this problem. Keynesian theory of economic equilibrium was born in the 1930s. XX century. Its founder is the English economist John Maynard Keynes. Keynesian theory began to spread after the Great Depression - a severe economic crisis that gripped the capitalist world in 1929-33. Keynes set out his theory in the book The General Theory of Employment, Interest and Money, which came into conflict with the then prevailing classical views on economics. It was generally recognized as truly revolutionary for its time. In his work, the important role of government intervention in economic life is substantiated.

In his book, Keynes presented a fundamentally new economic model and apparatus of economic analysis. Over time, his teaching developed and was supplemented by the achievements of world economic thought. It is currently an integral part of Keynesian theory.

The relevance and practical significance of the problem of macroeconomic equilibrium is determined by the possibility of practical application of the instruments of economic policy proposed by the supporters of the Keynesian approach. Many of the recommendations of the Keynesian school served as the basis for the economic policy of the governments of many states for several decades. There is no doubt that the experience of implementing Keynesian recipes for regulating the economy should be taken into account when carrying out economic reforms in our country.

In economic science, a fairly large volume of literature is devoted to this problem. Research on this topic was carried out both within the framework of the Keynesian school itself, and in other directions.

The purpose of this work is to consider the position of the Keynesian school on macroeconomic equilibrium. Based on the set goal, the following tasks are defined in the work:

- Consider the economic and mathematical models of macroeconomic equilibrium of Keynesian theory.

- Show the point of view of Keynesian theory on economic policy.

The work uses the terms and methods of analysis used in economic science. The method of equilibrium analysis, based on the circulation of income and expenses, is the basic one in the study of economic models of macroeconomic equilibrium. Keynes introduced into scientific circulation aggregated macroeconomic values that describe objects at the level of the national economy. By establishing quantitative relationships between them, there is a construction of economic and mathematical models - simplified descriptions of economic reality. Despite a certain amount of abstractness and models reflect all the significant factors of a particular problem and help to understand the functioning of economic mechanisms.

CHAPTER 1. THEORETICAL BASIS OF MACROECONOMIC BALANCE

1.1. Macroeconomic equilibrium concept

The problem of macroeconomic equilibrium is understood as the search for such a choice (which suits everyone), in which the way of using limited production resources (capital, land, labor) to create various goods and their distribution among different members of society are balanced. This balance means that cumulative proportionality is achieved:

a) production and consumption;

b) resources and their use;

c) supply and demand;

d) factors of production and its results;

e) material and financial flows.

Thus, macroeconomic equilibrium is a key problem in economic theory and economic policy of any state.

This conclusion is based on the fact that the ideal (theoretically desirable) balance is a stable use of the economic "energy" of individuals with the full optimal realization of their interests in all structural elements, sectors, spheres of the national economy.

It is obvious that equilibrium thus understood is an economic ideal, a system of abstractions of real life, albeit essential, but nevertheless. However, without this there is no science, because it studies not only the reasons for the discrepancy between essence and phenomenon, but also practice with the ideal.

1) empirical detection and recording of economic relations;

2) identification of essential connections within them;

3) precise quantitative determination of the conditions of equilibrium of the elements that make up the world of economic phenomena in accordance with the law of free competition.

Ideally (optimum), the achievement of the third stage expresses the goal of economic scientific knowledge. Moreover, following the logic of V. Pareto, the actual macroeconomic ideal is:

a) in theory - building a general equilibrium model of the economic system;

b) in practice - bringing the behavior of all consumers (buyers) and producers (sellers) in accordance with the requirements of the law of free competition.

In economic theory, the macroeconomic ideal is the construction of general equilibrium models of the economic system.

In real life, various violations of the requirements of such a model occur.

But the importance of theoretical models of macroeconomic equilibrium allows us to determine the specific factors of deviations of real processes from ideal ones, to find ways to implement the optimal state of the economy.

In economic science, there are many models of macroeconomic equilibrium, reflecting the views of different directions of economic thought on this problem:

F. Quesnay model of simple reproduction on the example of the economy France XVIII centuries;

K. Marx schemes of simple and extended capitalist social reproduction;

L. Walras model of general economic equilibrium in the conditions of the law of free competition;

V. Leontiev model “output costs”;

J. Keynes model of short-term economic equilibrium.

Macroeconomic equilibrium is the central problem of social reproduction.

Distinguish between ideal and real balance. (Fig. 1.1)

The ideal is achieved in the economic behavior of individuals with the full optimal realization of their interests in all structural elements, sectors, spheres of the national economy.

Achieving such an equilibrium presupposes the observance of the following reproduction conditions:

All individuals must find commodities in the market;

All entrepreneurs must find the factors of production in the market;

The entire product from last year must be implemented.

Fig. 1.1 Types of economic equilibrium

Ideal equilibrium proceeds from the prerequisites of ideal competition and the absence of side effects, which, in principle, is not realistic, since in the real economy there are no such phenomena as perfect competition and a clean market. Crises and inflation throw the economy out of balance.

Real macroeconomic equilibrium that is established in the economic system under conditions of imperfect competition and with external factors affecting the market.

Distinguish between partial and complete equilibrium:

Partial equilibrium is called equilibrium in a particular market of goods, services, factors of production;

Full (general) equilibrium is a simultaneous equilibrium in all markets, the equilibrium of the entire economic system, or macroeconomic equilibrium.

Full economic equilibrium is the structural optimum of the economic system, to which society strives, but never fully achieves it due to the constant change of the optimum itself, the ideal of proportionality.

1.2. Classical theory of macroeconomic equilibrium

It should be noted that before Keynes, general economic equilibrium was not considered an independent macroeconomic problem in economic theory. Therefore, the classical model of general economic equilibrium (GER) is a synthesized presentation of the views of the economists of the classical school using the modern terminological apparatus.

The classical OER model is based on the basic postulates of the classical concept, namely:

- The economy is presented as an economy of perfect competition and is self-regulating due to the absolute flexibility of prices, rational behavior of subjects and as a result of the action of automatic stabilizers. In the capital market, the built-in stabilizer is a flexible interest rate, in the labor market - a flexible nominal wage rate.

Self-regulation of the economy means that equilibrium in each of the markets is established automatically, and any deviations from the equilibrium state are caused by random factors and are temporary. The system of built-in stabilizers allows the economy to restore the disturbed balance independently, without interference from the state.

- Money serves as a counting unit and an intermediary in commodity transactions, but it is not wealth, that is, it does not have an independent value (the principle of money neutrality). As a result, the markets for money and goods are not interconnected and in the analysis the money sector is separated from the real one, to which the classical school refers to the markets of goods, capital (securities) and labor.

The division of the economy into two sectors is called the classic dichotomy. In accordance with this, it is argued that real variable and relative prices are determined in the real sector, and nominal variable and absolute prices are determined in the monetary sector.

- Employment, due to self-regulation of the labor market, is presented as complete, and unemployment can only be natural. At the same time, the labor market plays a leading role in shaping the conditions for the OER in the real sector of the economy.

Equilibrium in the labor market means that firms have achieved their output targets, while households have achieved income levels defined in accordance with the concept of endogenous income.

The production function in a short period is a function of one variable - the amount of labor, therefore, the equilibrium level of employment determines the level of real production, which is reflected in the third equation. And since employment is full (everyone who wanted to get a job at a given wage rate got it), the volume of production is fixed at the level of natural output, and the aggregate supply curve takes a vertical form.

The generated volume of the aggregate supply is the sum of the factor income of households, which are distributed by the latter for consumption and savings: y = C + S.

In order for an equilibrium to be established in the market of goods, the equality of the aggregate supply to the aggregate demand is necessary.

Since the aggregate demand in a simple model represents the sum of consumer and investment expenditures: y = C + I, then if the condition I = S is met, an equilibrium will be established in the market of goods. That is, according to Say's law, any supply generates a corresponding demand.

If the planned investments do not correspond to the planned savings, then an imbalance may arise in the market for goods. However, in the classical model, any such imbalance is eliminated in the capital market.

Equilibrium conditions in the capital market are reflected in the fourth equation. The parameter that ensures equilibrium in the capital market is a flexible interest rate.

If, for some reason, the planned volumes of savings and investments do not coincide at a given interest rate, then the economy begins an iterative process of changing the current interest rate to its value, which ensures a balance of savings and investment.

Graphically, the relationship between the rate of interest, investment and savings according to the "classics" is as follows (Fig. 1.2).

The graph shows an illustration of the equilibrium position between savings and investments: curve II - investment, curve SS - savings; on the ordinate axis the value of the interest rate (r); on the abscissa - savings and investments.

It is obvious that investment is a function of the rate of interest I = I (r), and this function is decreasing: the higher the level of the interest rate, the lower the level of investment.

Fig. 1.2 The classical model of the interaction between investment and savings

Savings are also a function (but already increasing) of the rate of interest: S = S (r). The level of interest equal to r 0 ensures equality of savings and investments on the scale of the entire economy, the levels r 1 and r 2 are the deviation from this state.

For example, suppose the planned savings were less than the planned investments.

Then in the capital market competition of investors for free credit resources will begin, which will cause an increase in the interest rate.

An increase in the interest rate will lead to a revision of the volumes of planned savings upwards and investments downwards, until such time as the interest rate is established, which ensures equilibrium.

When the volume of savings exceeds the volume of investment in the capital market, free credit resources are formed, which will cause a decrease in the interest rate to its equilibrium value.

That is, if an imbalance arises in the market of goods, then it is reflected in the capital market, and since the latter has a built-in stabilizer that allows restoring equilibrium, restoring equilibrium in the capital market leads to the restoration of equilibrium in the market of goods.

Thus, Walras's law is confirmed, according to which, if equilibrium is established in two (labor and capital) of three interconnected markets, then it is established in the third market - the market of goods.

The fifth equation stands alone and is only needed to determine the current price level.

Given the parameters of the money supply and the velocity of money circulation, the price level depends only on the parameter of the real national income: Р = (Mv) / y.

On the other hand, at the established equilibrium value of the real national income, the change in the parameters of the money market due to the neutrality of money is reflected only in the change in the price level.

If we represent the quantitative equation of exchange with respect to y and thereby express the aggregate demand function: y = (Mv) / P, then it is obvious that to ensure the condition y = const, it is necessary to change the money supply and the price level in the same proportion.

The neutrality of money is most fully illustrated by a mechanism called the "Cambridge Effect".

The fact is that each subject plans for himself some optimal level of cash (real cash). Economic entities perceive any change in the amount of money as a deviation of the value of real cash balances from the optimal value and take actions to restore its optimal value.

If the real cash register grows, the subjects begin to exchange surplus cash for goods, increasing consumer spending and aggregate demand; in the event of a decrease in the real cash register, aggregate demand decreases.

And since in conditions of full employment, the aggregate supply is rigidly fixed relative to the level of natural output, then its only possible response to a change in aggregate demand will be a corresponding change in the price level.

Prices in the classical concept are absolutely flexible, and therefore such a reaction of the aggregate supply to fluctuations in demand occurs instantly.

Price flexibility extends not only to goods, but also to factors of production. Therefore, a change in the level of prices for goods causes a corresponding change in the level of prices for factors. This is how the nominal wage changes, while the real one remains unchanged.

Consequently, the prices of goods, factors and general level prices vary in the same proportion.

The representatives of the classical school were characterized by microeconomic analysis, but their views and conclusions fairly accurately reflect the functioning of the market system.

It should be noted that the classics considered the general economic equilibrium only in the short term for conditions of perfect competition. Jean-Baptiste Say was the first to formulate the so-called "law of markets", the essence of which boiled down to the following statement: the supply of goods creates its own demand, or, in other words, the volume of products produced automatically provides income equal to the value of all created goods, and, therefore, is waste for its full implementation.

This means that, firstly, the goal of the owner of the income is not to receive money as such, but to acquire various material goods, i.e. the income received is spent in its entirety. With this approach, money plays a purely technical function that simplifies the process of exchanging goods. Secondly, only own funds are spent.

Representatives of the classical direction have developed a fairly coherent theory of general economic equilibrium, which automatically ensures equality of income and expenses at full employment, which does not contradict the action of Say's law.

The starting point of this theory is the analysis of such categories as the interest rate of wages, the level of prices in the country. These key variables, which, in the view of the classics, are flexible quantities, provide equilibrium in the capital market, labor market and money market.

Interest balances the supply and demand of investment funds; flexible wages balances supply and demand in the labor market, so that any prolonged existence of forced unemployment is simply impossible; flexible prices ensure the “cleansing” of the market from products, so that long-term overproduction is also impossible; an increase in the money supply in circulation does not change anything in the real flow of goods and services, affecting only the nominal values.

Thus, the market mechanism in the theory of the classics is itself capable of correcting imbalances arising on the scale of the national economy and state intervention is unnecessary.

The principle of non-intervention of the state is the macroeconomic policy of the classics, and the recommendations of modern economists - supporters of the neoclassical direction are based on the conclusions of the classical school. Graphic interpretation of general economic equilibrium in the classical concept is shown in Figure 1.3.

The third quadrant of the lower part of the figure shows the process of forming an equilibrium in the labor market, where equilibrium values of the real wage rate w "and employment N" are established. In the fourth quadrant, the equilibrium value of the national income y is determined by projecting the equilibrium value N * onto the production function.

Fig. 1.3 General economic equilibrium in the classical concept

The equilibrium value y "determines the aggregate supply function. The aggregate demand function is derived from the quantitative equation of exchange: y = (Mv) / P. A change in the amount of money affects only nominal variables, changing the current price level P. Accordingly, the graphs AD and W shift from the origin of coordinates with an increase in the money supply and vice versa with a decrease. The upper part of the figure shows the process of formation of equilibrium conditions in the capital market, where the equilibrium interest rate is set. So, the formation of conditions for general economic equilibrium in the classical model occurs according to the principle of self-regulation, without government intervention, which is ensured by three built-in stabilizers: flexible prices, flexible nominal wage rates and flexible interest rates, while the monetary and real sectors are independent of each other.

CHAPTER 2. MODELS OF ECONOMIC BALANCE D. KEYNES

2.1. Aggregate cost model

The key point in Keynesian theory is the concept of aggregate spending. Aggregate expenses - the sum of all expenses of economic entities for goods and services produced in the economy. The components of total costs are:

- Consumer demand.

- Business demand.

- State demand.

- The demand of the rest of the world.

Consumer demand. Represents consumption expenditure by households. Including the costs of durable goods, non-durable goods, service costs.

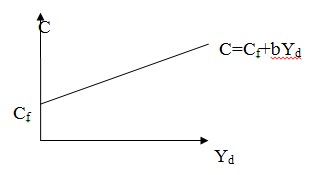

According to Keynesian theory, the consumption function has the form:

Where C f is autonomous consumption, independent of income,

Y d - disposable income, income after taxes Y-T,

b - marginal propensity to consume; coefficient that shows how much of the additional income goes to consumption.

The consumption function graph is shown in Figure 2.1.

Figure 2.1. Consumption function graph

Savings are the portion of income that is not currently consumed. The consumption function is:

where S f - autonomous saving, independent of income,

Y d - disposable income,

s - marginal propensity to save; coefficient that shows how much of the additional income goes to savings.

The main factor that determines the amount of consumption and savings is disposable income. In addition, taxes, accumulated wealth, expectations, and consumer debt affect consumption and savings. It is considered that the graphs of the consumption and savings functions are stable. This is because consumption and saving are strongly influenced by habits and traditions.

Business demand - investment costs of firms. These include: manufacturing investment, housing, changes in inventories.

Investment demand is the most volatile part of aggregate demand. The reasons for this are cyclical fluctuations in output, the volatility of the economic environment, the irregularity of innovations, and the long terms of use of fixed assets.

The investment function looks like:

where I f - autonomous investments determined by external economic factors and independent of income,

d is the coefficient of sensitivity of investments to changes in interest rates,

i is the real interest rate.

Investment volume and interest rate in Figure 2.2. are inversely related. The higher the interest rate - the payment for the loan provided, the fewer investment projects will be implemented.

Autonomous investments can be supplemented by stimulated (induced) investments, which increase with the growth of GNP. Taking into account the dependence of investments on income, the function takes the form:

where g is the marginal propensity to invest - the part of the additional income that goes to the investment.

Figure 2.2. Investment schedule

Factors affecting the size of investments - the expected rate of net profit, the real interest rate, taxes, changes in production technologies, the size of the fixed capital of enterprises, economic expectations, income, etc.

State demand (public procurement) - all expenses of federal, regional and local authorities for the purchase of final products and services. These are expenses for defense, security, social and cultural events, assistance to scientific and technological progress, public administration, etc. However, this excludes transfer payments - gratuitous payments by the state, as not directly related to production.

To finance its activities, the state levies taxes through legislation.

The tax function is:

where T f - taxes independent of income,

t is the tax rate.

The state budget is approved by parliament for the current fiscal year in advance, and the main items of government spending remain unchanged. The change in the size of expenses is associated with a lengthy procedure for discussion in parliament. Thus, the amount of government spending in the total expenditure model is assumed to be constant.

Rest of the world demand is net exports; the amount by which foreign export costs exceed domestic import costs. The pure export function looks like:

where v is the marginal propensity to import; part of the additional income that is spent on imports,

X f stands for offline net export.

The relationship between the income of a given country and its net exports is negative, because with the growth of income, imports increase, and exports do not depend on income and remain unchanged.

Aggregate cost model. Planned expenditures (E) - the amount that macroeconomic entities plan to spend on goods and services. Real costs differ from projected costs when firms make unplanned investments.

Figure 2.3. Equilibrium in the total cost model

On the Y = E line, the production level is equal to the planned costs. When the schedule of planned expenditures is shifted up or down by some amount, the change in the value of output will be somewhat larger. This is due to the multiplier effect.

The equilibrium volume of production in the aggregate cost model is determined by the intersection point of the bisector Y = E and the aggregate demand graph in Figure 2.3. The total cost model is applied in the case of fixed prices.

Inflow and outflow method allows you to identify the reasons for the inequality of total spending and GDP. Inflows are understood as any addition to consumer spending - investment, government procurement, export earnings. Outflows - expenses not aimed at purchasing products manufactured in the country - savings, taxes, import costs.

The method is as follows. Part of the disposable income is not spent on consumption, but may be spent on savings, taxes, and imports. Therefore, consumer spending alone is not enough to purchase the entire volume of products. But the expenditures of the state, firms and exports are added to consumption, which make up for the lack of consumer spending. Therefore, achieving equilibrium requires equal outflows and inflows (I + G + EX = S + T + IM).

2.2. Aggregate Demand Model - Aggregate Supply

Aggregate demand model - aggregate supply is a macroeconomic equilibrium model. Macroeconomic equilibrium is achieved when aggregate demand and aggregate supply are equal.

Aggregate demand. Aggregate demand is the expenses of households, firms, the state and the rest of the world for the purchase of products manufactured in the country. The magnitude of each component of aggregate demand varies over time to varying degrees. Thus, government purchases are the most stable part, their size changes relatively slowly.

The graphical representation of the model is a curve with a negative slope (Figure 2.4). The aggregate demand curve AD = C + I + G + X n shows the number of goods and services that consumers are willing to purchase at every possible price level. At each of its points, the commodity and money markets are in a state of equilibrium.

Fig. 2.4. Aggregate demand curve.

The negative slope of the curve reflects the inverse relationship between the general price level and the value of aggregate demand. This is due to the following price factors.

Wealth effect - when prices rise, the purchasing power of financial assets decreases and economic agents reduce costs. Interest rate effect - a high price level with a fixed supply of money causes an increase in the demand for money and an increase in the interest rate. An increase in interest rates reduces investment. The effect of import purchases - with an increase in prices for domestic goods, consumers switch to their foreign counterparts. Changes in price factors are graphically reflected by the movement along the aggregate demand curve.

Non-price factors affecting aggregate demand - consumer welfare, consumer expectations, taxes, interest rates, subsidies, political environment, technology development, etc. Changes in these factors will be reflected in the graph by a shift in the aggregate demand curve to the right or to the left.

Aggregate supply. Aggregate supply is the amount of final goods and services produced in the economy for a certain period in monetary terms. The aggregate supply curve shows how much goods and services can be offered by producers at each possible price level.

Non-price factors of aggregate supply: production technologies, consumer welfare, taxes, resource prices, etc.

There are different points of view regarding the shape of the aggregate supply curve in economics. The classical school of economists believes that the curve is vertical at the level of full employment of factors of production. At the same time, prices and nominal wages, according to the classic economists, are flexible. This ensures a quick restoration of equilibrium in the economic system. The classical model is more consistent with the behavior of the economy in the long run.

Keynesian theory, in addition to the vertical segment of the aggregate supply curve, considers horizontal and ascending segments (Figure 2.5). The fundamental difference from the classical model is that the economy operates under conditions of underemployment; prices, nominal wages and other nominal values are “rigid”.

Fig. 2.5. Aggregate supply curve.

The reasons for the "rigidity" of wages and prices - the operation of labor contracts, the statutory minimum wage, the effect of the "menu", the duration of contracts for the supply of products, the intervention of trade unions. With an increase in demand, firms increase output without changing the price level or changing it insignificantly.

The horizontal segment of the aggregate supply curve characterizes the state of the economy in recession - a high level of unemployment and a significant underutilization of production capacities. With an increase in aggregate demand, firms are able to increase production without increasing prices.

In the upward segment, an increase in the real volume of output is accompanied by an increase in prices. The positive slope of the curve shows the direct dependence of the output on the price level. An increase in aggregate demand will cause both an increase in prices and an increase in production volumes.

In the upward segment, the economy is close to full employment. To increase output in response to the expansion of aggregate demand, firms attract additional resources. Factor prices rise, costs rise, and firms are forced to raise product prices.

The shape of the aggregate supply curve allows you to observe the change in production costs per unit of output when the volume of output changes. In the horizontal segment, resources are available to firms at constant prices and production increases without price increases. In the upward segment, production costs rise, and the overall price level in the economy rises. In the vertical segment, the possibilities for increasing output have been exhausted, since all resources are occupied. The expansion of aggregate demand will only lead to higher prices. Firms can buy up resources already occupied, increasing their production costs and increasing output. But on the whole, real output in the economy will not increase.

Macroeconomic equilibrium is the equality of aggregate demand and aggregate supply. A graphic illustration of this equality is the intersection point Y r of the curves of aggregate demand and aggregate supply in Figure 2.6. At this point, all the national product produced will be bought.

Figure 2.6. Equilibrium in the AD-AS model

Keynesian theory assumes that macroeconomic equilibrium can be achieved at any segment of the aggregate supply curve. In the horizontal segment, equilibrium is achieved without inflation, in the ascending segment, with a slight increase in prices, and in the vertical segment, in conditions of inflation.

The equilibrium volume of output changes with a shift in the curves of aggregate demand and aggregate supply. The result of an increase in aggregate demand depends on the state of the economy. The multiplier effect on different segments of the aggregate supply curve acts in different strengths.

On the horizontal segment, the effect of the multiplier is manifested in full. The increase in total costs causes a significant increase in output at a constant price level. However, in the ascending and vertical segments, changes in aggregate demand will be absorbed to some extent by inflation.

Due to the inflexibility of prices in the short term, a reduction in aggregate demand in the ascending and vertical segments will lead to their fall only after a certain time.

Shrinking aggregate supply - A shift in the aggregate supply curve to the left will reduce output and cause prices to rise In such a situation, cost inflation arises. An increase in aggregate supply indicates economic growth, output increases and prices fall.

2.3. Macroeconomic Equilibrium in the Money Market

Demand for money. The demand for money is the desire of economic entities to have a certain amount of means of payment at a certain point in time. Keynesian theory of demand for money is different from classical theory. If in the classical theory the demand for money depends on income, then in Keynesian demand is mainly associated with the interest rate.

In his book A General Theory of Employment, Interest, and Money, Keynes considered three motives that lead people to hold financial assets in the form of money: the transactional, the precautionary motive, and the speculative motive.

The transactional motive L t is associated with the need for money for planned purchases and payments. In this case, the demand for money is directly proportional to the amount of income and does not depend on the interest rate.

Precautionary Motive L p - Explains keeping money in case of contingencies. The demand for money also depends on the amount of income, but the influence of the interest rate is felt.

As you can see, both of these motives in the Keynesian theory of demand for money determine its some similarity with the classical theory.

The speculative motive differs significantly from the previous two. The Keynesian model assumes that an economic entity has assets in two forms - money and bonds. Speculative demand is based on the inverse relationship between the interest rate and the bond rate.